The Death and Resurrection of TV

About TV dying, content thriving and the different ways audiences are being drawn in to a streaming future

Tune in folks.

We’re looking at the death of Pay-TV and the opportunities for it’s resurrection. Today you’ll learn about the devastating affects that Covid has had on Pay-TV viewership, the ways that streaming platforms are capitalising on a migrating audience and how the streaming world isn’t a battle, but a party.

It’s 2020, which means we are celebrating the 10th birthday of the decline in Pay-TV Penetration:

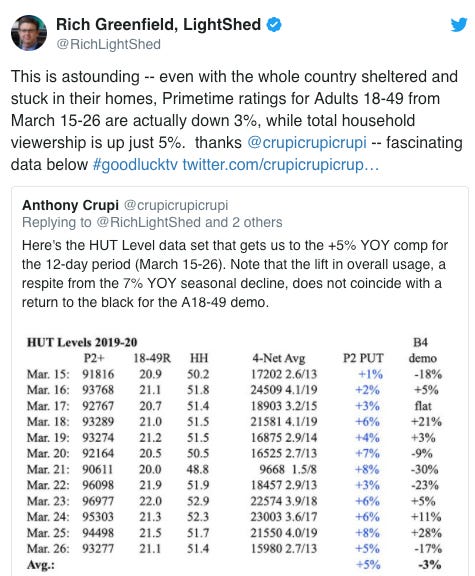

If the last 10 years has been rough on Pay-TV, 2020 has been an absolute disaster:

Let’s look at why Covid hasn’t buoyed Pay-TV’s numbers as it rationally should:

Live sports is a crucial and unique driver for Pay-TV (no football on Netflix!) without live sports, audience numbers drop. The bad news long term is that Post-Covid it’s likely sports leagues will start to sign deals split between linear + digital rights rather than exclusives on Pay-TV. NFL already started this with Amazon’s simulcasts. So Pay-TV’s big audience magnet won’t have the same reliable pull in the future.

Pay-TV is the largest recurring entertainment expense for the average household. Less discretionary income is leading people to abandon cable, forcing Pay-TV networks to lean harder into their streaming spin-offs.

Pay-TV broadcasting is built around our normal work day hours (i.e prime shows from 7, less popular programming during the day) this doesn’t suit our current ‘always at home’ routine. On demand streaming does, for example I can watch a prime time show at 3pm (when I’m supposed to be creating ad campaigns).

Streaming temptations

In addition to Covid factors, streaming platforms have become experts at tempting audiences away from Pay-TV. Let’s look at three key strategies used to migrate audiences.

1) Become the biggest giant in the room

Netflix outspends and outsmarts it’s way to the top

In 2019 they spent $2.6B in marketing, up from $2.3B the year before. Netflix has an incredible level of brand AND show awareness. This means that the majority of spending can be focused on customer acquisition marketing, putting them in a remarkably strong position to grow their audience.

Netflix also outspends other platforms on original content. Last year $15B was spent on original content, double the spend of Amazon Prime and triple the spend of HBO and Hulu. This commitment to content attracts new customers with shows that can’t be found anywhere else, and their original and exclusive offerings justify subscription costs to current customers, hooking them into the platform.

Netflix’s famously effective recommendation algorithm is built to keep audiences engaged. Crucially the AI component of this algorithm gets better with more user data. This means that as the Netflix audience grows, it’s ability to keep that audience watching improves with time.

2) Leverage a well established brand

Disney+ is a great example of using an established brand to draw in a mass audience:

Looking at the established brand power of Disney, their incredible launch starts to make sense:

A crucial challenge when launching a streaming service is creating trust in the brand’s platform. Even if Quibi has recognisable and loved shows, because they aren’t a known and trusted entertainment brand they have to do a lot of work (and spend over $500m) to create awareness and consideration for the platform. Disney is probably the most loved entertainment brand globally, driven by generations of nostalgia and milestone experiences both on and off the screen. This means they can focus on building acquisition and promoting their product. The hard brand building work has been done for decades.

Disney’s ecosystem allows them to leverage a wide spread of ‘brand tentacles’ to draw various audiences in. Anyone who has been to one of their theme parks, seen a Disney movie or played a Disney video game can be tapped on the shoulder to sign up for the service. This takes a lot of the legwork out of migrating audiences to the platform.

Disney’s established quality of content and the unique experience that content delivers makes their value argument stronger. The magic of Disney originals are universally recognised. It took Netflix almost a decade, and billions of dollars, to convince the world that their originals were worth watching. Disney content own this reputation from day one.

3) Offer irresistible value

Offering a free, ad-supported option is the avenue I find most interesting. It’s also the most reliable method for Pay-TV channels to step into the streaming game. I’ll use NBCUniversal’s new streaming platform Peacock as an example.

A free service allows new entrants to circumnavigate the streaming wars. Netflix is often framed as a killer of Pay-TV, or a killer of smaller streaming platforms. By offering a free service you aren’t competing for audience dollars, and therefore can be additive to a viewers primary platform subscription, rather than an alternative choice. Peacock will never be able to spend as much as Netflix on marketing, or originals, but when a platform is free audiences don’t have to make that choice. This allows free platforms like Peacock to gain easy admission into the streaming game, and was one of the reasons they were able to gain 10 million sign ups within 3 months of launching.

An ad-supported services extends the value out of cable programming. Looking at Peacock’s programs you can see they host many shows already funded through their Pay-TV parent’s channel. By creating an ad-supported streaming platform not only can they capture audiences lost to streaming, they can also create additional revenue from ads, without having to spend big on new original programming.

A platform like Peacock leverages a proven customer acquisition technique: The ‘Freemium’ model. The model works by bringing in customers to a light, or ad-supported, version of a service, building user behaviour over time, and then offering a premium version once the value of the product has been justified to customers. This has been successfully deployed by a range of services from Spotify to Evernote. As customers cut cords and once our volatile economy settles, one can expect audiences to pay for a service like Peacock in addition to their main streaming subscription as it’s still cheaper than a Pay-TV bundle.

It’s not a battle, it’s a party

As more viewers cut the cord and move to streaming the category will look less like a battle and more like a party. Netflix will always be the extrovert taking up the most energy in the room, but it doesn’t need to be beaten to be successful. A smaller slice of an ever-growing pie means that Pay-TV networks, and their streaming platform spin-offs, can remain successful as long as they continue to offer value, and quality, to audiences.

Writer’s note: If you’re liking my newsletter, and know someone who will find it interesting, feel free to forward it along